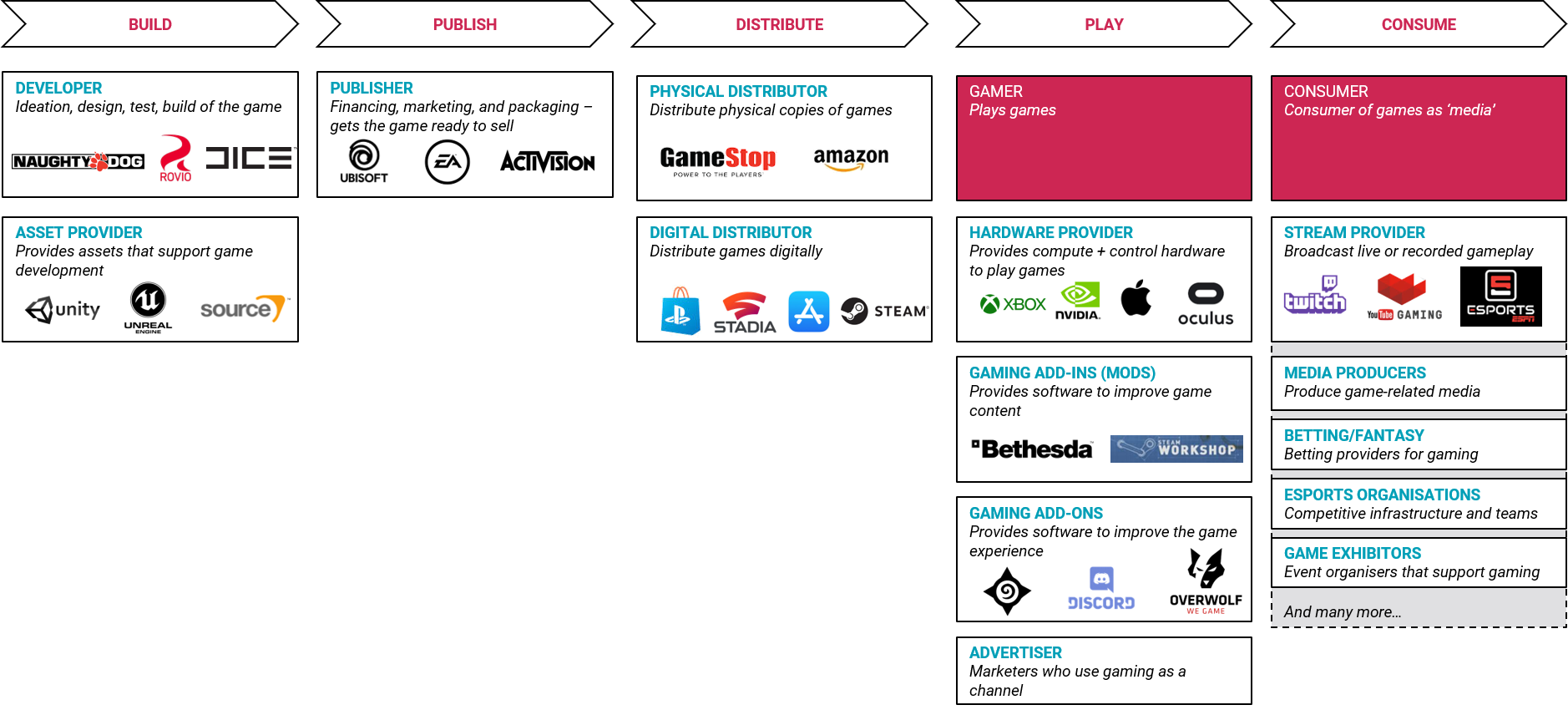

Where US$150 billion actually goes

Gaming is a behemoth of an industry that generates revenues over $150 billion per year.

That's bigger than the music and box office industry combined.

Consider the top movie release to date, Avengers: Endgame. When it premiered, it made over US$858m during its opening weekend.

It failed to outperform the highest-grossing game in history, Grand Theft Auto V's release back in 2013, which earned US$1 billion in just over three days.

Across its lifetime -- Endgame has generated in the vicinity of US$2.2 billion. GTA V? North of US$6 billion.

With that much money being thrown around, it stands to reason that there are a lot of actors involved -- and I've done my best to simplify it to the actors in the lifecycle of developing a single game.

Note: several companies act in multiple roles. E.g. EA is vertically integrated to act as a developer, publisher, and distributor through its Origin platform. The intent of this map is to show the variety of actors in the industry -- follow-up posts will cover the strategies some of them are making across this value chain.

Stages of the game lifecycle

The following is an overview of each actor in the gaming industry. It should be noted that this is a heavily simplified version and each actor described faces their own unique challenges in the area they operate in.

The build stage

Developer

Historically, game developers have been independent operators that build games from the ground up.

Constructing a game involves writing the story, designing the game mechanics, programming these game rules, and developing the art that gives the game life.

Game developers can range from individual developers who build from their bedroom to large development agencies with hundreds of staff members.

Developers win through creativity and strength of their intellectual property -- e.g. Codemasters is known for its racing game engine and strong pedigree in building racing games.

Many game developers are now owned by game publishers. E.g. DICE is owned by EA which made Battlefield.

Asset provider

Asset providers are parties who provide resources to support and accelerate game development. They can range from providing full-fledged game engines -- e.g. Unreal Engine -- to being independent providers of simple art assets -- e.g. TurboSquid.

For the purpose of this map, we'll consider the primary asset providers to be game engine developers. The biggest actors here include Unreal, Unity, and Amazon Lumberyard who aim to offer a one-stop-shop for game developers through their engines and integrated asset stores.

These providers aim to profit from revenue-share of games built using the platform and/or licensing fees, as the engines are typically offered free.

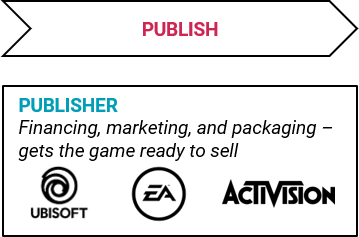

The publishing stage

Publisher

Publishers are the money, might, and marketing behind the game developers.

They make it possible for developers to get their game out to the market to be able to generate sales.

Publishers pay developers cents on the dollar for every dollar made selling to consumers -- in most large-scale productions they take the lion's share (60+%) of wholesale top-line revenue. The numbers vary drastically based on the size of the game and distribution method in question (e.g. digital only).

Publishers make money like movie production houses do. They take on massive risks with the hopes that they strike gold once in a while. Significant risks they take on include:

- Slippage -- if the developers miss their (typically tight) deadlines for some reason, publishers lose the value of any marketing they'd spent promising a "Christmas" launch and excited gamers lose interest, which typically leads to a muted release.

- Game reception -- if the game isn't liked by gamers, sales will be hard to come by. Related to this is that publishers sometimes have to pay royalties to console manufacturers for "manufactured" games as opposed to "sold" games like every other industry -- and any under-performance to projected sales results in lost money.

Most large game publishers also own development studios to gain more control over the development lifecycle and minimise risk. Publishers are notorious for "stifling" creativity by bringing development studios in-house to work on stale sequels. (For a movie example -- think Home Alone 3.)

The distribution stage

Physical distributors

Likely the easiest to intuitively understand, physical distributors make sure the game is accessible for gamers.

The perfect example here is GameStop who at their peak had over 5,500 stores around the world dedicated to selling new and second-hand physical games, consoles, and merchandise.

It shouldn't come as a surprise to anyone that physical retailers and GameStop are facing tough times as digital distribution has grown. (Think Blockbuster replaced by Netflix.)

Physical distributors make profits (see: losses) through buying in wholesale from publishers and marking up games for sale to gamers.

Digital distributors

Digital distributors for games refers to the likes of PlayStation Store, Nintendo eShop, Microsoft Store, Google Play, Apple App Store, Steam, and Origin -- i.e. providers who let you access games online.

If you're familiar with the names above, you'll notice that there are a few categories of digital distributors -- mobile-based distributors (e.g. Apple App Store), console-based distributors (PlayStation Store), and PC distributors (Steam).

Digital distributors are similar to physical distributors in that they make money by taking a share of the sales from the consumer. They typically achieve this by clipping around ~30% of the sale price before passing on the revenue to the publisher -- as opposed to buying game discs wholesale from the publisher and marking up the price.

Digital distribution is where things get interesting due to the variety of actors trying to capture the market across a variety of platforms -- including new actors such as Google Stadia who use cloud gaming as their differentiator.

I do this for the love of writing — each subscriber costs me money. But please subscribe anyway and spread the word.

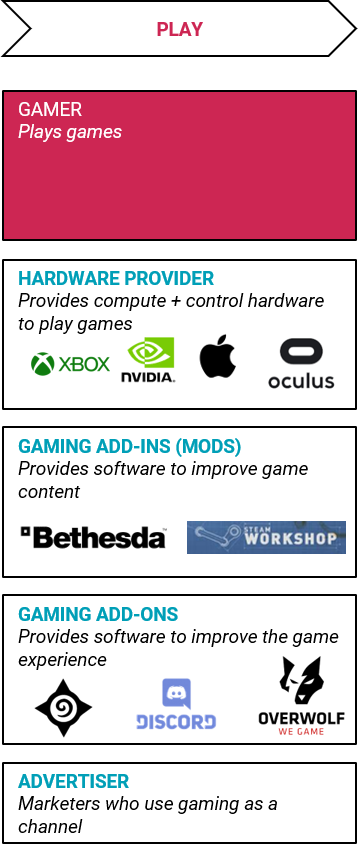

The playing stage

This stage is the most over-simplified portion of this map. Every single participant here supports the "playing" of games in drastically different ways and I will cover this in future articles -- for now, this simplification should work to set the frame for future discussion.

Gamer

This is who the entire industry is centred around. The game player, the one who drives the demand for the market.

Notably, as the industry has developed over the decades -- it should be noted that gamers span more than the preconceived notion of teenage boys. Games are played by a wider range of people than ever before and span PC, console, and mobile.

The 6-year old boy playing Minecraft is a gamer.

So is the 83-year-old grandmother who can't get enough of Candy Crush Saga on her iPad.

On top of simply buying and playing games -- gamers can create communities that improve the long-term value proposition of a game. This works well for developers and publishers as an active community usually equals loyal players who will keep coming back for more.

EVE Online is a game that has been active for over 15 years and is known for its million-dollar wars (yes, real money) and deep community that keeps its small-but-loyal fanbase coming back for more.

Hardware provider

Covering a broad range of suppliers -- consoles (e.g. Xbox, PlayStation), graphics cards (e.g. NVIDIA, AMD), mobile (e.g. Apple, Samsung, Razer), and many many others.

This bucket encapsulates providers who supply "compute" power to be able to play the game and hardware to be able to "control" the game.

There are several combinations of compute + control. For example:

- PlayStation 4 is manufactured by Sony. The DualShock controller acts as the "control". The "compute" is in-built using AMD, Samsung, and Panasonic components amongst others. The control could easily be swapped for a Logitech steering wheel for a racing game.

- In the case of an iPhone, the compute and the control are the same device.

- On a PC, the control is typically a keyboard and mouse (offered by a number of manufacturers), and the compute can be made in any one of millions of combinations through custom-built PCs that use a variety of components (e.g. a NVIDIA graphics card, Intel processor etc.).

Note: There is a subset of hardware providers that don't meet the above definition, and we can classify these as "peripherals" -- e.g. headsets, gaming monitors, gaming chairs, etc.

Gaming add-ins (mods)

This group includes a wider variety of actors -- from individual developers to marketplace providers who offer software assets to improve and/or modify the game content.

An example of this would be developers building mods that offer custom weapons. Steam Workshop allows developers to sell mods at any price they wish -- and started off with the highly-billed The Elder Scrolls V: Skyrim where individual developers can build and offer weapons, graphics changes etc.

The idea here is to insert code "in" to the game to change the experience, as contrasted by an "add-on" which runs alongside the game.

Most mods are harmless -- e.g. cosmetic, or superpowers for offline play.

However, some mods are unfair or against the Terms of Service for a game by nature -- e.g. an "aimbot" that automatically targets enemies during online play for easy wins -- and are typically policed by a combination of the gamer community and publisher. There have been several multiplayer games that have seen dwindling usage due to the prevalence of unregulated cheating through mods.

Money is made on mods by the developers of the mods, at times in combination with distributors such as Steam claiming a share of revenue and distribution rights.

It should be noted that a majority of mods are free and created by gamers for other gamers out of love for the game. Publishers try to limit the provision of mods for the purposes of their revenue model -- e.g. League of Legends makes money by selling in-game skins (cosmetics) and stands to lose money if they open up the ability for all users to create skins freely.

Think of mods as the custom sound system made by 3rd parties that go in your car.

Gaming add-ons

Add-ons operate with much more freedom compared to add-ins as they are not subject to strict Terms of Service and/or IP protection that publishers may enforce.

I've defined them here as software that supplements your game experience. Some examples:

- Discord -- which could be simplified to "Slack for gaming" -- offers voice-chat rooms, chat, and gamer-specific community features.

- Poker indicators -- that offer insight into the probabilities you are facing to save you from the mental load of calculating your outs.

- Overwolf -- offers a toolset to build add-ons such as "overlays" that display useful information to gamers about what's happening in the game. Hearthstone Deck Tracker is an example of an overlay -- providing a visual record of all the actions an opponent has taken in a game. (Think of "move history" in Chess.)

Add-on developers make money through sales. Typically, this is either a one-off licence purchase or an on-going subscription for premium features.

Advertisers

Love them or hate them, wherever you direct your attention -- advertisers will find a way there to try and sell you the coolest new toy that your life will just not be complete without. I've got advertisers across both "play" and "consume" because it doesn't matter to the advertiser what you're doing -- as long as their brand can get in front of you, they will be willing to advertise.

Advertisers in gaming range from household brands (e.g. Coca-Cola) to gaming-specific brands (e.g. SteelSeries).

Advertising in gaming is best compared to advertising in sports. You can have advertising across professional teams as sponsors, in-game, across televised broadcasts and more.

A notable difference between gaming and other industries is that gaming is almost entirely digital-based. You'll seldom see newspaper ads for a video game.

This requires advertisers to get creative to capture the attention of an audience that's more tech-savvy than most other industries.

As an example -- from personal experience founding and running Cloth5.com, a League of Legends site that served over a million views per month on average -- a huge challenge we had to overcome was that standard display ads on webpages were simply not profitable enough as gamers used ad blockers almost twice as much as the average web user.

The consumption stage

There are a variety of actors in this stage and it would be a non-trivial task to try and list them all, so I'll keep it simple.

Consumer

A secondary cornerstone of the gaming industry is the "consumer". A vague term designed to encompass non-player consumers.

Think of these as fans who may not necessarily play the game. E.g. if you're a basketball fan, even though you're not necessarily a basketball player, you do consume live broadcasts, sports articles, analysis etc. and contribute your hard-earned money to support the sport.

In a gaming context, this could be anything from watching individual streamers on Twitch as your nightly viewing to being a cosplay artist at a convention.

Your place in the gaming industry is non-trivial. Consumers play one key role above all others.

They provide the attention that can be monetised through ads -- e.g. supporting professional eSports players, organisations, and tournaments handing out millions of dollars in prize money.

Stream provider

Think of these as broadcasters for a comparison to the analog world. If you want to watch basketball -- you go to ESPN. If you want to watch Overwatch, you can go to Twitch, YouTube, or one of many other actors (including ESPN's eSports arm).

It's important to note that there is a significant market for both "live" and "recorded" gameplay streams.

Revenue is generated here by platform providers by partnering with advertisers and offering premium features to consumers of this content. The two leaders here are undoubtedly Amazon (Twitch) and Google (YouTube) -- in the Western market at least.

Media producers

While this category spans a wide range of content, there is one important callout.

A significant difference between the analog world of traditional media and gaming is that it is extremely easy for any gamer or consumer to create content and broadcast it -- about as easy as it is to upload a photo or video to Facebook. There is no additional cost for expensive camera rigs, studio set-ups, etc. for a video format that's based in a CGI world -- all you need is a computer or a console to render the game.

This means that powerhouse publishers are often competing with individual creators on top of the usual corporate actors.

The most popular individual streamers on platforms such as Twitch can command the attention of over 100,000 viewers at any one time and net 7-figure incomes.

Individual YouTubers can average millions of views for videos of recorded gameplay paired with their webcam.

It should be noted that media production in gaming isn't related to purely gameplay streams -- there is a wealth of content created for each game ranging from gameplay guides, information databases, and analysis to eSports reporting, artwork, and opinion pieces. All of which operate differently between games -- i.e. the leading news source for one game may not even be an actor for a different game.

This leads to heavy fragmentation in content production and several niches that producers can try to win in.

On the flipside, with the ability to easily create and compete, there is also a glut of content being produced every minute -- which makes gaming one of the toughest industries to compete in.

eSports organisations

Competitive infrastructure and organisations form a huge portion of the growth story for gaming.

The easiest way to explain eSports is to use the example of well-known sporting leagues -- let's use football (soccer).

Let's compare European soccer to League of Legends. (This is a very simplified view of it.)

- The eSports infrastructure is primarily controlled by Riot Games, the developer and publisher. (FIFA in soccer.)

- They create regional leagues around the world for teams to compete in -- Europe, North America, Oceania etc. (Premier League, La Liga etc.)

- Teams compete in these leagues with the hopes of winning their regional title and earning a ticket to compete for the world championship.

- The world championships are broadcast worldwide (as are the regional tournaments) to millions of viewers with millions of dollars in prize money up for grabs. (Champions League.)

- Sponsors try to target consumers by supporting tournaments and teams with advertising. (E.g. Coca-Cola.)

eSports is a promising entertainment medium as viewership for events such as the world championship in League of Legends rivals that of the Super Bowl (in a specific metric anyway).

Where eSports gets exciting is that League of Legends is simply one game in the eSports sub-industry. There are several other games with flourishing and active competitive activity -- e.g. Fortnite, Counterstrike, Hearthstone, Overwatch, and many many more.

Other "consume" actors

There are several other actors on the consumption side of gaming -- ranging from online betting providers (e.g. bet365) to game exhibitors (e.g. PAX) that support the industry.

I've chosen not to expansively detail them as they are not required to form a strong understanding of the gaming industry.

What's next?

Now that you've been introduced to the gaming industry and understand the map, we can explore the latest in gaming in more depth.

I'll be aiming to cover key moves in the gaming market and discuss the strategic implications -- both for the organisations in question and gamers impacted.

I hope you'll enjoy this journey with me.

Disclaimer: Thoughts are my own and do not represent any other parties.

Newsletter

I do this for the love of writing.

Each subscriber costs me money, but please do it anyway and spread the word. Monthly at most.

You might also like

Mobile gaming's missing brain

Every studio tracks ARPDAU, ROAS, retention curves. None of them answer the question actually worth asking -- which specific player is about to churn.

AI shopping is years away. The infrastructure isn't.

When the AI does the buying, value migrates from attention to delegation. Stripe's five level map shows where commerce is today and what changes at Level 4.

The Codification Treadmill

The person who replaces you probably won't be AI. It'll be someone from the next department over who learned to use it.